2024 was a busy year for the U.S. power sector with a number of significant policy advancements in renewables, transmission, nuclear energy and other areas.

The year ahead will undoubtedly be an active one, too, as the sector navigates ongoing business challenges and the impacts of the 2024 elections. Here are nine key issues to watch in 2025.

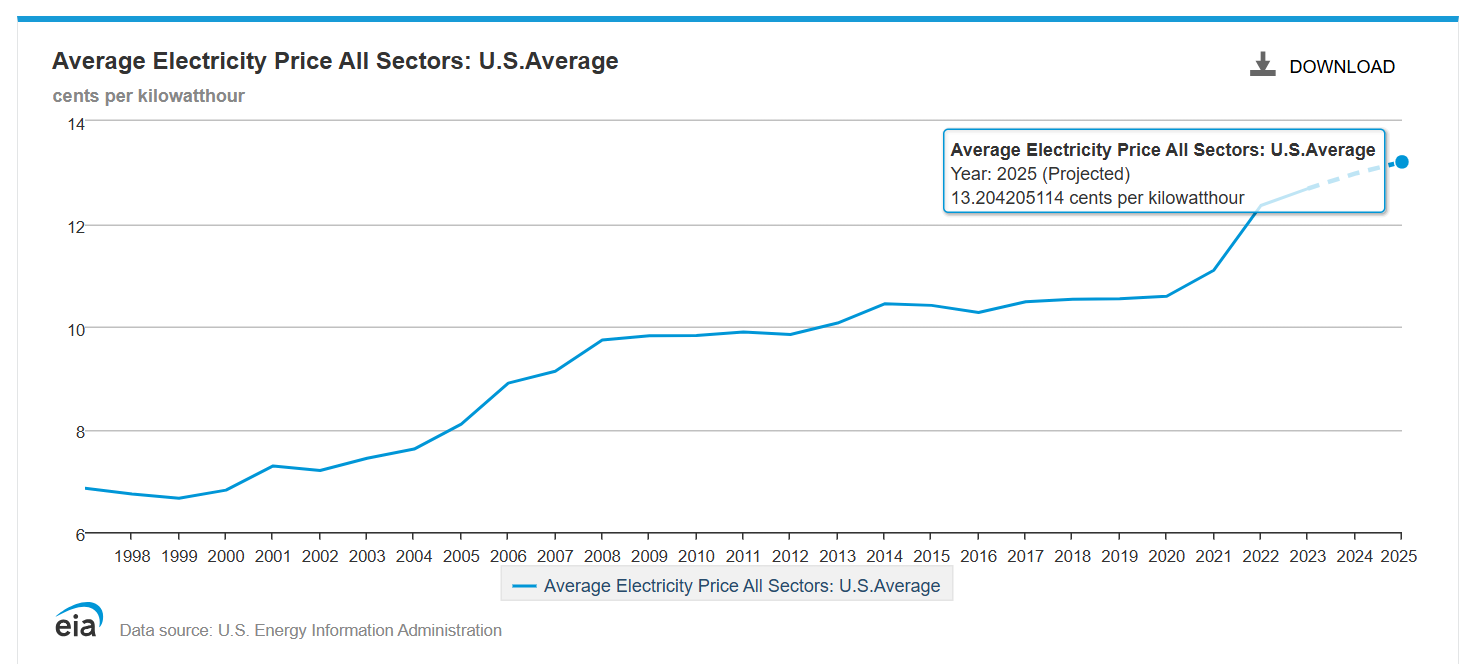

Electricity prices continue perpetual ascent, driven by demand and gas exports

The price U.S. consumers pay for electricity will continue to ascend in 2025, driven by a range of factors including rising demand, transmission and distribution cost increases, and an anticipated rise in the price of natural gas, experts say.

Across all customer classes, U.S. electricity prices are expected to average 13.2 cents/kWh in 2025, up from 12.68 cents/kWh in 2023, according to data from the U.S. Energy Information Administration. Residential electricity prices across all regions will average 16.7 cents/kWh in 2025, up from 15 cents/kWh in 2022.

“Both transmission and distribution cost increases are driven by decarbonization and that is expected to continue nationwide,” Paul Cicio, chair of the Electricity Transmission Competition Coalition, said in an email.

Natural gas prices were low in 2024 but as liquefied natural gas export terminals come on-stream in late 2025 and in 2026 and more U.S. natural gas is shipped out of the country, “we expect higher natural gas prices and resulting higher electricity prices,” Cicio said.

U.S. LNG exports have tripled over the past five years, are expected to double again by 2030 and could increase even further under existing authorizations, Secretary of Energy Jennifer Granholm said in December.

The rise in natural gas exports is also a threat to reliability, Cicio said, “because there is inadequate natural gas pipeline capacity on a regional basis, to add generation.”

The increased LNG exports are happening at a time when building and transportation electrification, data center growth, artificial intelligence, cryptocurrency mining and battery and fuel cell manufacturing are contributing to higher electricity consumption and rising electricity prices.

U.S. electricity demand is projected to grow 9% by 2028 and 18% by 2033, an increase of 2% per year, on average, relative to 2024 levels, consulting firm ICF said in a September report. Peak demand could grow 5% over the next four years, ICF said.

Rising demand threatens reliability as 2025 kicks off with grid warnings

The North American Electric Reliability Corp. rang in the New Year with a stark call to action for the electric power sector, signaling years of warnings may now be an immediate threat.

“I’m asking everyone in the electricity supply chain … to take all appropriate actions,” NERC CEO Jim Robb said in a Dec. 31 recorded address, ahead of the cold weather now blanketing parts of the United States.

After nearly two decades of stagnant electricity demand growth, the United States is seeing data centers and electrification drive consumption higher. Combined with generator retirements and a changing resource base, the nation’s grid reliability watchdog says this is a perilous moment for the power system.

Data centers could account for 44% of U.S. electricity load growth from 2023 to 2028, Bain & Co. said in an October analysis. U.S. utilities are facing “potentially overwhelming demand,” the consulting firm said.

NERC published an assessment in December concluding more than half of the U.S. electric grid could see energy shortfalls in the next five to 10 years, particularly under extreme weather conditions. Peak summer demand is forecast to rise by more than 122 GW in the next decade, adding 15.7% to current system peaks, NERC said, while generation retirements of up to 115 GW are possible by 2034.

Federal policies are needed to support energy production, manufacturing and infrastructure, according to National Rural Electric Cooperative Association CEO Jim Matheson. NERC’s report “continues painting a grim picture of our nation’s energy future and growing threats to reliable electricity,” he said.

NERC said it is now worried about the potential for arctic cold to bring extremely low temperatures, damaging winds, snow and freezing rain to Midwestern, Eastern, and Southern states.

“NERC is especially concerned about natural gas supply given the significant amount of [gas] production in the mid-Atlantic and Northeast,” the reliability organization said in a Dec. 31 warning

Natural gas producers have taken “a multitude of proactive measures to prepare for winter weather so that we can provide safe and reliable service to our customers,” according to Natural Gas Supply Association President and CEO Dena Wiggins.

Grid operators plan market changes amid challenging supply/demand dynamics

Making sure there is enough power supply to meet the growing needs of U.S. energy users is one of the top issues facing the operators of U.S. wholesale power markets.

With demand forecasts growing sharply for the first time in years, grid operators like the Midcontinent Independent System Operator are working to ensure their markets send appropriate signals to spur new generation while also working to unclog their interconnection queues.

The PJM Interconnection may be facing the most challenges as it is trying to overhaul its capacity market amid warnings that it may soon face major supply shortfalls.

PJM has for several years taken steps to reform its capacity markets — which led to capacity auction delays and a condensed auction schedule — but the record-high prices of its last capacity auction in July sparked unprecedented turmoil.

The auction will cost ratepayers across the grid operator’s footprint $14.7 billion for the delivery year that begins in June, up from $2.2 billion in the previous auction. Since the results were released, at least three market-related complaints were filed at the Federal Energy Regulatory Commission, PJM has proposed a one-time, fast-track process for shovel-ready projects and more market changes are in the works.

Other grid operators are responding to similar supply/demand challenges. MISO, for example, in November proposed, for a second time, setting a megawatt cap on its annual interconnection queue to limit its study size, as well as exemptions to the cap.

Meanwhile, the California Independent System Operator and the Southwest Power Pool are planning to expand wholesale markets in the West. CAISO aims to launch the Extended Day-Ahead Market in 2026 while SPP plans to start its Markets+ initiative in 2027, pending approval of the tariff by FERC.

Renewables sector is cautious but determined heading into Trump’s second term

In 2025, ongoing load growth in the U.S. will continue driving demand for renewable energy, while the sector simultaneously faces uncertainty due to President-elect Donald Trump’s vow to prioritize fossil fuel-based generation.

Beyond the incoming administration, connecting renewable energy to the grid remains a challenge, with wind and solar constituting the vast majority of capacity in interconnection queues across the country. A lack of sufficient transmission to deliver renewable energy to where it’s needed is also seen as a key challenge. Congress has been considering bipartisan permitting reform legislation that aims to facilitate transmission buildout, but the prospects for such legislation remain uncertain.

Advanced Energy United President and CEO Heather O’Neill said the renewable energy industry is currently “stymied” by bottlenecks, “whether it’s interconnection or siting.”

Despite federal uncertainty, work to solve these bottlenecks is ongoing at the state level, O’Neill said – bolstered by the Federal Energy Regulatory Commission’s Order 1920, which affirmed states’ role in transmission planning, and by emerging solutions to get more out of the current power system like grid-enhancing technologies.

“We know we need to build more, but we also know that we can get a heck of a lot more out of the existing transmission grid,” she said. “When we talk to governors, their staff, commissioners – they want to attract economic development in their state.”

Felisa Sanchez, a partner with law firm K&L Gates’ maritime and finance groups, said that permitting reform legislations could play a significant role if Trump attempts to block offshore wind projects.

“One of the big, key ways that Trump could affect projects is by delaying that permitting process over the next four years,” she said.

While Trump’s reelection and his strong anti-offshore wind stance have created concerns for the offshore wind industry, Sanchez said project developers “are still engaged in these conversations with the understanding that even if there is a slowdown or a halt to the industry, they anticipate being able to pick up again in four years.”

Trump is expected to implement even stricter tariffs in his second term, including on imported solar components, which could increase costs and contribute to supply chain constraints. However, as solar technology advances and domestic supply grows to meet demand, prices continue to drop.

NRC reforms expected to benefit nuclear industry amid policy uncertainty

From game-changing federal legislation, to groundbreaking on what could be the United States’ first new grid-connected non-light-water reactor in decades, to commitments by some of the world’s biggest tech companies to power data centers with existing or next-generation reactors, 2024 was a busy year for the U.S. nuclear industry.

Momentum for nuclear energy gathered amid rapidly rising projections of future load growth due to the electrification of buildings and transport, reshoring and decarbonization of heavy industry, and above all, the expected proliferation of power-hungry AI models.

“2024 was the year that we all woke up to the need for nuclear,” said Craig Piercy, CEO of the American Nuclear Society. “2025 is the year we really get down to serious business.”

A reinvigorated U.S. Nuclear Regulatory Commission will be instrumental, experts say. More than a dozen advanced reactor developers are engaging with the NRC on licensing-related matters, “but licensing timelines and costs remain uneven, often attributable to inconsistent quality in mundane but important practices,” Nuclear Innovation Alliance Executive Director Judi Greenwald said in a December paper.

In 2025, the agency must continue work on the new, technology-neutral Part 53 licensing framework as Congress holds it accountable for implementing ADVANCE Act provisions like lower application fees, early-mover prizes and hiring incentives to expand its own workforce, Greenwald said.

Developers of smaller-scale reactors, like Oklo and Last Energy, could begin to benefit in 2025 from an ADVANCE Act provision that establishes an 18-month licensing timeline for microreactors and may enable even faster approvals for subsequent microreactor license applications.

“The NRC has acknowledged that these timelines are doable,” said Ryan Duncan, vice president of government relations at Last Energy.

While it remains to be seen if the Trump administration will aim to maintain current funding levels for emerging nuclear technologies, the U.S. Department of Defense is likely to remain “very interested” in procuring nuclear reactors for on-base resiliency and could advance initiatives announced by the U.S. Army, Navy and Air Force, Duncan said.

In the civilian world, Holtec could reactivate its 800-MW Palisades nuclear generating station in Michigan by the end of 2025, the company said last fall. Meanwhile, utilities are looking at about 2 GW of uprate opportunities to “wring as much performance out of the existing fleet as possible” and may propose additional nuclear capacity — possibly SMRs at existing nuclear or coal power sites — in integrated resource plans published this year, Piercy said.

Declining battery costs may counter tariff risk as emerging storage technologies look to break out

The United States installed 3,806 MW/9,931 MWh of energy storage in Q3 2024, and the industry is on track for 30% growth in storage deployments for the full year, Wood Mackenzie and the American Clean Power Association said in December.

Though Wood Mackenzie sees annual deployment growth decelerating to 10% from 2025 to 2028 due to “early-stage development constraints,” the industry has powerful tailwinds, including recent and expected future declines in battery input costs and ambitious storage procurement targets in states like New York, California and Massachusetts. Increasingly, state storage procurements focus on installations capable of full-power discharge over durations longer than four hours.

“No one in their right mind would bet against longer and longer duration energy storage at lower cost,” said Intersect Power CEO Sheldon Kimber, whose company in December announced plans to colocate gigawatt-scale wind, solar and battery plants with Google data centers beginning later this decade.

Non-lithium technologies like Form Energy’s iron-air and CMBlu’s redox flow battery are more economical for discharge durations beyond approximately four to eight hours, experts say. Form expects to commission a 1.5 MW/150 MWh commercial demonstration project in Minnesota later this year as it expands its West Virginia factory to meet near-term demand.

The potential for higher tariffs on imported lithium-ion battery components could benefit emerging storage technologies with simpler, easier-to-onshore supply chains, including iron-air, Kimber said.

But “lithium-ion has a huge head start [and it will be] hard to overcome that leadership position,” especially with lithium battery costs expected to decline further, said Mark Repsher, partner and energy markets expert at PA Consulting.

Load growth prompts states, utilities to embrace virtual power plants

Only 19.5%, or 33 GW, of total North American distributed energy resource capacity — residential and commercial solar arrays and batteries, electric vehicles, smart thermostats, water heaters and more — is enrolled in a virtual power plant, according to a July report from Wood Mackenzie. Smart thermostats alone could provide up to 70 GW of dispatchable VPP capacity, said Renew Home CEO Ben Brown.

Inadequate policy, overcomplicated program design and technological challenges conspire to slow uptake, Wood Mackenzie said. But DER experts interviewed by Utility Dive are optimistic that the tide is turning as load growth outpaces generation capacity additions.

“[Utilities] are running out of levers to flip to keep up with capacity and demand,” said Viridi CEO Jon Williams.

In November, Renew Home and NRG announced plans to deploy a 1-GW smart thermostat VPP in Texas by 2035. The following month, the Electric Reliability Council of Texas proposed a doubling of capacity in its aggregated distributed energy resource pilot program. In addition, the Electric Power Research Institute is leading two initiatives to advance common DER interoperability standards.

In 2025 and beyond, state policy could take center stage with DERs, Brown and Williams said. With most parts of the U.S. distribution grid running well below full capacity outside of peak periods and an average five-year wait for bulk interconnections, Williams said policymakers should incentivize distribution-connected energy storage over new transmission-connected generation assets.

“You can’t just add a gas plant because you’re too lazy to use technology,” Williams said.

In October, California Gov. Gavin Newsom, D, ordered the California Public Utilities Commission and other state agencies to find ways to reduce electricity bills in a move that could pave the way for CPUC to set new targets and incentives for utilities to adopt VPPs and make it easier for consumers to get rewarded for participating in VPPs, Brown said.

FERC, DOE advance major transmission policies as permitting, other challenges remain

2024 saw several major developments in U.S. transmission with more to come in the year ahead as new policies move closer to implementation.

“With increased load from AI and other drivers, and resource adequacy needs as highlighted by NERC’s 2024 Long Term Reliability Assessment, transmission will continue to play a key role in meeting these needs as cost effectively as possible,” said Christina Hayes, executive director of Americans for a Clean Energy Grid.

In terms of interregional transmission, the Federal Energy Regulatory Commission on Nov. 21, largely upheld its Order 1920 on transmission planning and cost allocation, first issued in May, but gave state regulators a bigger role in shaping scenario development and cost allocation. Grid operators must now file plans with FERC indicating how they will comply with the order.

In addition, on Oct. 3, the Department of Energy released the National Transmission Planning Study, which provides a framework for interregional transmission development.

Siting and permitting issues have been a persistent challenge for new transmission. While permitting reform legislation failed to pass in 2024, efforts will continue in the next Congress.

“It will be incumbent upon policymakers to streamline regulatory processes and actively and effectively incentivize investment in new transmission if meaningful progress is to be made on building a robust and modernized grid,“ said Larry Gasteiger, executive director at WIRES.

“The prior Trump administration took significant steps to streamline siting and permitting; the Biden administration pushed a number of individual projects over the finish line and issued [Coordinated Interagency Authorizations and Permits] rules on implementing section 216(h) of the Federal Power Act,” Hayes noted.

Some key questions around transmission, according to Hayes, include “how will the next administration support siting and permitting of transmission through the federal process …. Will it support backstop siting in FERC’s Order No. 1977? What else will this administration do to support siting and permitting of transmission projects?”

Momentum, private sector expected to drive electrification in 2025

The last four years have seen a major push to electrify building and transportation systems, with federal incentives helping to drive the popularity of heat pumps and electric vehicles. But with a second Trump administration set to begin this month, supporters of the shift away from fossil fuels are counting on momentum and the private sector to continue progress.

“As we move into the deployment phase and the implementation phase, it’s going to be more and more important that folks are using that money well,” said Jeff Allen, executive director of Forth, a nonprofit focused on EV adoption. “That’s probably going to be a lot of the funding you have to live off, for the next few years.”

“There’s also going to be a lot more people looking over your shoulder,” Allen said, speaking during a Dec. 17 webinar focused on the outlook for electrification.

Through the Infrastructure Investment and Jobs Act and the Inflation Reduction Act, President Biden has made billions available to support the clean energy transition. Heat pump incentives have been rolled out on the state-level and more than half of the authorized funds will be distributed to the states before Trump takes office, experts say.

But Trump has talked about ending EV tax credits, which can total up to $7,500 per vehicle. The incentives helped push sales of EVs to almost 9% of U.S. light-duty vehicle sales in the third quarter of last year.

JD Power in August said it expects EV sales to achieve a 36% market share by 2030.

“I do think we’re going to see some of these tax incentives really come under fire,” said Lynda Tran, CEO of Lincoln Room Strategies.

But the bulk of the EV transition work will continue, Tran said, with the private sector continuing to ramp up investments in clean energy manufacturing. “They’re planning to double down,” she said.

Development of EV charging infrastructure is also key.

The $5 billion National Electric Vehicle Infrastructure program authorized by the IIJA aims to install thousands of EV chargers around the country but relatively few have been rolled out so far, said Ryan McKinnon, spokesperson for the Charge Ahead Partnership. “The slow pace has turned the program into a poster child for sluggish federal bureaucracy,” he said.

If the NEVI program is scaled back “it will not have a major impact. Businesses that are poised to turn a profit, gain new customers and expand into a new revenue stream will continue to build, own and operate EV charging stations.”